-

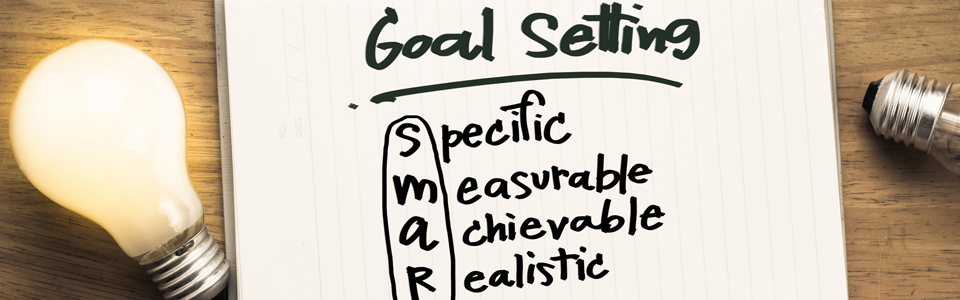

Set S.M.A.R.T. Goals

Saving tends to be easier when you have a certain purpose in mind: Saving for your first house, your retirement at a certain age, a child’s college education, or even a trip around the world. The important thing is for your goals to be specific, measurable, actionable, realistic and time-bound, or SMART.

To develop a sound plan, these goals must have both a time frame and a dollar amount that is measurable. Once you have listed and quantified your goals, you need to prioritize them. You may find, for example, that saving for a new home is more important than buying a new car.

Whatever your objective, be specific. Figure out how many weeks or months there are between now and when you want to reach your target. Divide the estimated cost by that number to make it actionable. That’s how much you’ll need to save each week or month to have enough money set aside. Ask yourself, is this realistic? Remember, a goal is a dream with a deadline.

-

Pay Yourself First

Save and invest 5-10% of your gross annual income. Of course, this can be much harder than it sounds. If you’re currently living from paycheck to paycheck without any real opportunity to get ahead, begin by creating a solid spending plan after tracking all monthly expenses.

Once you figure out how you can control your discretionary spending, you can then redirect the money into a savings account. For many people, a good way to start saving regularly is to have a small amount transferred automatically from their paycheck to a savings account or mutual fund. The idea: If you don’t see it, you don’t miss it.

-

Maintain an Emergency Fund

Before you commit your newfound savings to volatile and hard-to-reach investments, make sure you have at least three to six months’ worth of expenses saved in an emergency fund to see yourself through difficult times. Keeping it liquid will ensure that you don’t have to sell investments when their prices are down, and guarantee that you can always get to your money quickly.

If you have trouble deciding how much you need to keep on hand, begin by considering the standard expenses you have in a month, and then estimate all the expenses you might have in the future (possible insurance deductibles and other emergencies). Generally, if you spend a larger portion of your income on discretionary expenses that you could cut easily in a financial crisis, the less money you need to keep on hand in your emergency account. If you have dependents, you’d want to keep more money in your emergency fund to offset the greater risk.

-

Pay Off Your Credit Card Debt

If you’re trying to save while carrying a large credit card balance at, say, 19.8%, realize that paying off the debt is a guaranteed return of nearly 20% per year. Once you pay off your credit cards, use them only for convenience, and pay off the balance each month. If you tend to run up credit card charges, get rid of the credit card and go back to using cash, checks and a debit card.

-

Insure Your Family Adequately

A major lawsuit, unexpected illness or accident can be financially devastating if you lack proper insurance. The key to insurance is to cover only financial losses so large that you could not cope with them and remain financially fit (known as the law of large numbers). If someone is dependent on your income, you need adequate life insurance. Long-term disability coverage is important as long as you need employment income. Also, be sure to carry adequate liability coverage on your home and auto policies.

To save on annual premiums, it might be feasible for you to raise your insurance deductible, or eliminate dual coverages. And whenever purchasing insurance—life, home, disability, or auto—be sure to shop around, and buy only from a reputable firm.

-

Buy a Home

According to the U.S. census, since 1968, the median price of new single-family homes has gone up almost tenfold; many houses still appreciate at a rate of 6% to 8% annually. Further, homeownership entitles you to major tax breaks. Interest on first and second home mortgages is fully deductible, meaning Uncle Sam helps subsidize your property investment. Additionally, the equity in your home can be a great source of retirement income.

-

Take Advantage of Tax-deferred Investments

If your employer has a tax-deferred investment plan like a 401(k) or 403(b), use it. Often, employers will match your investment. Even if they don’t, no taxes are due on your contributions or earnings until you retire and begin withdrawing the funds. Tax-deferred savings means that your investments can grow much faster than they would otherwise. The same is true of IRAs, although the maximum amount you can invest annually in an IRA is substantially less than what you can put in a 401(k) or 403(b).

-

Diversify Your Investments

When it comes to managing risk to maximize your return, it pays to diversify. First you need to diversify among the three major asset classes: cash, stocks and bonds. Once you have decided on an allocation strategy among these three investment classes, it is important to diversify within each asset. This means buying multiple stocks within a variety of industries and holding bonds of varying maturities. Simply put, don’t put all your eggs in one basket.

All investments involve some trade-off between risk and return. Diversification reduces unnecessary risk by spreading your money among a variety of investments. Aside from diversification, the single most effective strategy is to invest continuously over time, with a long-term perspective.

-

Write a Will

The simplest way to ensure that your funds, property and personal effects will be distributed according to your wishes is to prepare a will. A will is a legal document that ensures that your assets will be given to family members or other beneficiaries you designate. Having a will is especially important if you have young children because it gives you the opportunity to designate a guardian for them in the event of your death. Although wills are simple to create, about half of all Americans die intestate, or without a will. With no will to indicate your wishes, the court steps in and distributes your property according to the laws of your state. If you have no apparent heirs and die without a will, it’s even possible that the state may claim your estate.

To begin, take an inventory of your assets, outline your objectives and determine which friends and family you wish to pass your belongings to. Then, when drafting a will, be sure to include the following: name a guardian for your children, name an executor, specify an alternate beneficiary and use a residuary clause which typically reads “I give the remainder of my estate to …” Once your will is drafted, you won’t have to think about it again unless your wishes or your financial situation changes substantially.

Source: Balance Financial Fitness

Comments Section

Please note: Comments are not monitored for member servicing inquiries and will not be published. If you have a question or comment about a Quorum product or account, please visit quorumfcu.org to submit a query with our Member Service Team. Thank you.